Harry Markowitz, the Nobel Prize-winning economist who pioneered modern portfolio theory, famously described diversification as the only free lunch in investing. His insight was simple: combining assets whose returns are not closely correlated can reduce risk without sacrificing expected return.

In practice, however, many portfolios that appear diversified are increasingly exposed to the same underlying drivers.

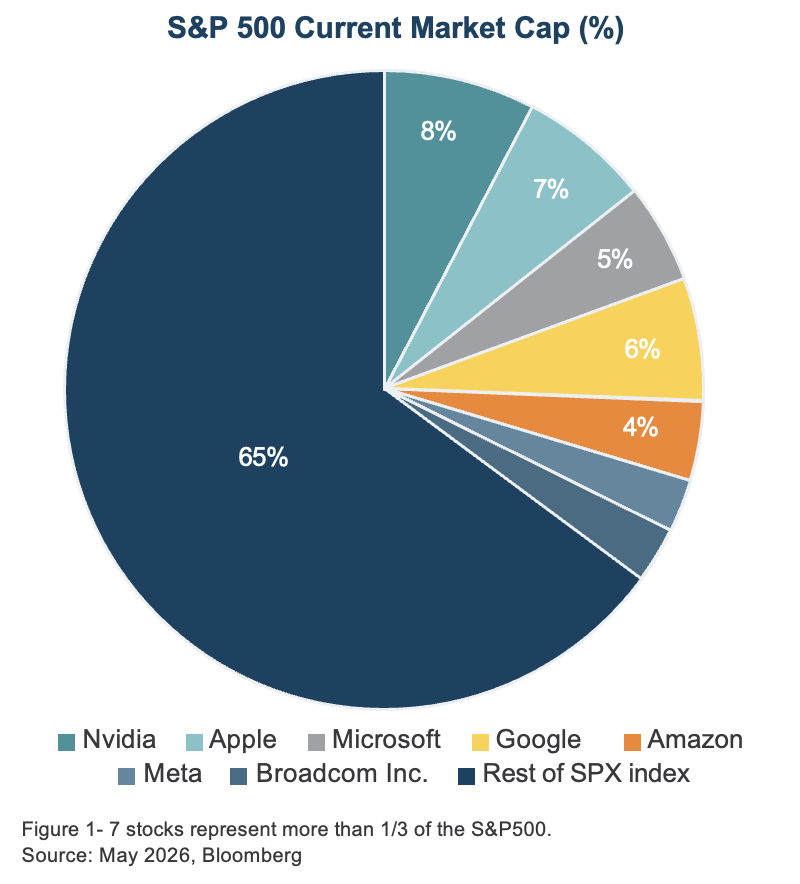

Global share markets have become more concentrated, particularly in the United States, where a small group of very large technology companies now represents a significant portion of major indices. Investors holding broad market index funds may assume they are widely spread across sectors, regions and opportunities, but much of their portfolio performance can still be driven by the same handful of companies.

Passive investing has accelerated this dynamic. Capital is allocated by index weight rather than valuation or fundamentals, creating a feedback loop where rising prices attract more capital, further increasing concentration. While often seen as a conservative approach, this can leave investors with greater exposure to the most expensive parts of the market and more reliance on continued optimism.

This creates a hidden risk. When markets are rising, concentration can feel rewarding. But when sentiment shifts, portfolios with too much exposure to the same companies, sectors or economic assumptions can fall together.

True diversification is not simply about holding more investments. It is about ensuring those investments behave differently under different market conditions.

Diversification works because different asset classes carry different primary risks. Equities compensate for economic uncertainty, credit for default risk, and government bonds for inflation and duration risk. When these risks are genuinely distinct, diversification is effective. When they are not, assets that appear different on paper can still move in unison.

Investors saw this clearly in 2022, when both equities and bonds declined together. What was expected to provide balance instead moved in the same direction.

A resilient portfolio should aim for exposure to genuinely different sources of risk and return. That may include balancing growth assets with income-producing investments, active conviction rather than pure index alignment, and maintaining liquidity and flexibility when conditions change.

Diversification is not about owning more of the same. It is about reducing reliance on any single outcome.

In a market shaped by higher interest rates, geopolitical uncertainty, and elevated valuations, that distinction matters more than ever.

Often, the greatest risk is not what investors can see, but what they assume they already have, or what they think they have avoided.